Beyond Bitcoin's Decline: Bitcoin Market Trend Research Report 2026

- Beta.B

- Jun 10

- 6 min read

Beta.B Group Releases Investor Behavior & Long-Term Market Outlook Report

Based on exclusive interviews with Mrs.Mariya Ebirayim, Managing Partner & Chief Strategy Officer

June 9, 2026 Beta.B Group

For informational purposes only. Not financial advice. Please refer to important disclosures on the final page.

EXECUTIVE SUMMARY

Bitcoin has entered a period of significant price correction, prompting renewed debate among investors about the asset's long-term viability. Beta.B Group releases this independent market research report drawing on exclusive interviews with Mariya Ebirayim, Managing Partner & Chief Strategy Officer, and a comprehensive review of on-chain data, ETF capital flows, mining economics, and institutional investor behavior.

This report contends that the central question for long-term investors is not where the price stands today, but whether the structural foundations of Bitcoin's investment thesis remain intact — and whether the current correction represents systemic breakdown or an expected phase of institutional market maturation.

Key Finding

"This correction is structurally different from 2018 and 2022. The critical question is not where prices stand today, but whether the market itself is transitioning into a new phase of institutional maturity."— Mariya

MARKET SNAPSHOT

The following data reflects market conditions as of the date of this report.

Bitcoin Price | Significant correction from cycle highs; trading in the vicinity of $60,000. Source: CoinGecko, June 2026 |

ETF Capital Flows | Sustained net outflows, concentrated in short-term trading capital. Quarterly ETF inflows of approximately 50,000 BTC — the lowest level recorded since the launch of U.S. spot Bitcoin ETFs. Source: Standard Chartered Research Note, Geoffrey Kendrick, December 2025 |

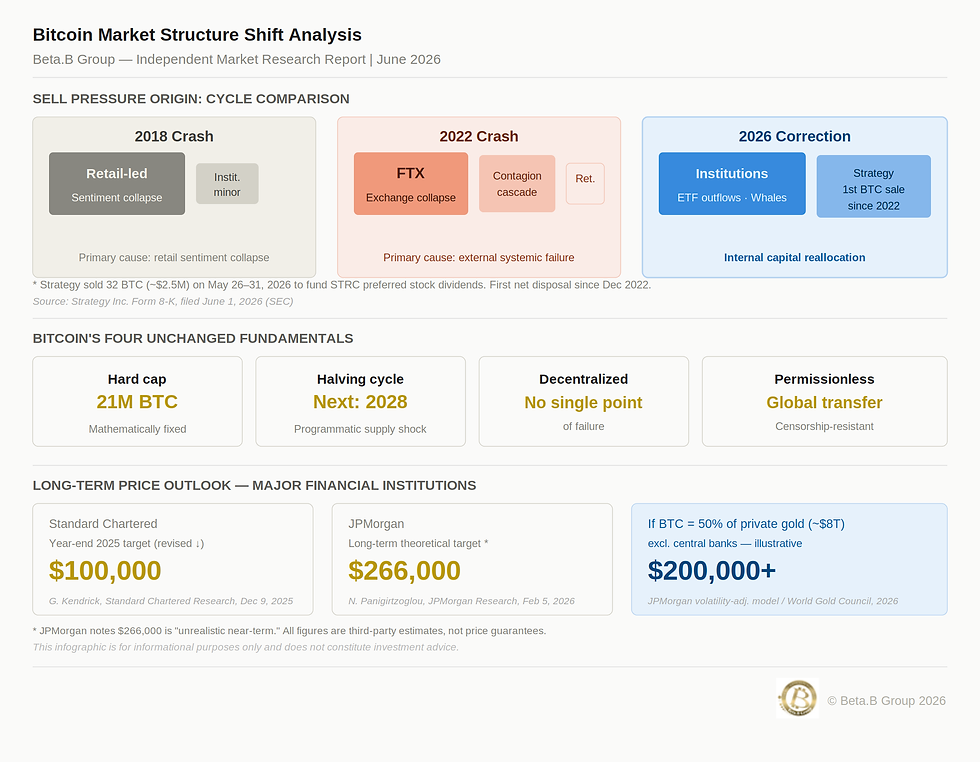

Strategy Inc. | May 26–31, 2026: first net Bitcoin disposal since December 2022. 32 BTC sold at an average of $77,135 per coin (~$2.5M). Proceeds allocated to STRC preferred stock dividend obligations. Remaining holdings: 843,706 BTC (0.0038% of treasury sold). Source: Strategy Inc. Form 8-K, SEC Filing, June 1, 2026 |

Mining Economics | Net daily revenue for major mining operations approaching the estimated production cost floor of approximately $87,000 per BTC. Source: JPMorgan Research, N. Panigirtzoglou, February 2026 |

Market Sentiment | Broad shift toward caution and risk-off positioning across both retail and institutional participants. Source: Beta.B Group proprietary analysis |

I. The Structural Shift in Sell-Side Pressure

What Sets This Correction Apart from 2018 and 2022

Understanding the nature of a market correction requires identifying its origin. The 2018 downturn was driven by the collapse of retail speculative demand. The 2022 correction was precipitated by systemic contagion — the implosion of FTX and its cascading effects across the digital asset industry.

The current cycle presents a materially different picture. Rather than an external shock, sell-side pressure originates from within the institutional layer itself:

– Coordinated position reductions by major holders

– Sustained net outflows from Bitcoin spot ETFs, concentrated in short-term trading capital

– Strategy Inc.'s first net Bitcoin disposal since 2022 — 32 BTC sold between May 26–31, 2026, at an average of $77,135 per coin (~$2.5M total), to fund STRC preferred stock dividend payments; 843,706 BTC remain on the balance sheet

(Source: Strategy Inc. Form 8-K, SEC Filing, June 1, 2026 / CoinDesk)

This is not the market breaking down under external pressure. It is capital reallocation occurring within a maturing market structure — a process that produces short-term volatility while laying the groundwork for deeper institutional liquidity over time.

"The identity of the sellers has changed. This is not market collapse — it is a shift in the market's center of gravity. Historically, such shifts precede an expansion of the price ceiling."— Mariya

II. Reading ETF Capital Flows Accurately

Short-Term Trading Capital vs. Long-Term Allocation Capital

Interpreting ETF outflows as a straightforward indicator of bearish institutional sentiment is an oversimplification. The capital flowing through Bitcoin ETFs comprises two structurally distinct pools with materially different behavioral profiles:

– Short-term trading capital — opportunistic, momentum-driven, and quick to rotate out during periods of volatility

– Long-term allocation capital — structurally committed, driven by investment mandate and portfolio strategy rather than day-to-day price action

The outflows currently observed are consistent with the exit of the former. Core holdings of major ETF issuers — including BlackRock and Fidelity — show no evidence of material reduction at this time. Long-term allocation capital is in a period of deliberate observation, not structural exit.

(Source: BlackRock iShares Bitcoin Trust / Fidelity Wise Origin Bitcoin Fund public disclosures, 2026)

"ETF flows do not represent the aggregate intention of all institutional investors. You have to assess the quality of the capital, not just the volume."— Mariya

III. Has Bitcoin's Investment Thesis Been Impaired?

Distinguishing Price Decline from Fundamental Value Erosion

A decline in price is not equivalent to an impairment of fundamental value. The core structural pillars of Bitcoin's investment thesis remain fully intact:

– Hard supply cap of 21 million coins — mathematically immutable

– Halving mechanism — programmatic supply shock recurring approximately every four years; next event scheduled for 2028

– Decentralized network architecture — no single point of failure or centralized control

– Permissionless global settlement — censorship resistance as a structural property

History offers a relevant precedent. When gold futures markets launched in 1974, institutional entry was widely criticized as corrupting the asset's integrity. Gold was trading at approximately $180 per ounce at the time. It has since surpassed $3,300. Institutional participation is a feature of asset maturation — not evidence of structural compromise.

(Source: World Gold Council, Gold Price Historical Data, 2026)

"The question investors should be asking is not how far prices have fallen, but whether the fundamental investment thesis has been impaired. As of today, the evidence does not support the latter conclusion." — Mariya

IV. Cycle Position & Long-Term Price Outlook

Institutional Frameworks and Structural Reference Points

On-chain data and mining economics suggest that current conditions exhibit characteristics consistent with the late stages of prior bear market cycles. The exit of marginal miners is approaching completion — a signal that has historically appeared in the final phases of Bitcoin downturns before structural recovery begins.

The following long-term price frameworks have been published by major financial institutions. These are analytical models, not guarantees of future performance:

Standard Chartered | Year-end 2025 target: $100,000. Long-term target: $500,000 by 2030. Note: revised from original $200,000 year-end target, citing slower-than-expected institutional adoption via ETFs. Source: Standard Chartered Research, Geoffrey Kendrick, December 9, 2025 |

JPMorgan | Long-term theoretical upside: $266,000, based on a volatility-adjusted comparison of Bitcoin's market cap to private-sector gold investment. The bank notes this target is 'unrealistic in the near term' but reflects structural long-term potential once negative sentiment reverses. Source: JPMorgan Research, N. Panigirtzoglou, February 5, 2026 |

Gold Parity Model | Private-sector gold investment totals approximately $8 trillion. If Bitcoin were to reach 50% of that figure on a volatility-adjusted basis, the implied per-coin price would exceed $200,000. Source: JPMorgan volatility-adjusted model, Feb 2026 / World Gold Council |

These projections are based on each institution's respective analytical assumptions and do not constitute price guarantees. This report similarly does not seek to predict specific price targets — its purpose is structural analysis and the provision of a reference framework for investment decision-making.

"A market bottom is not a price point — it is a process. What investors need in this environment is not forecasting precision, but a clear and coherent analytical framework."— Mariya

COMMENTARY

Markets grow through cycles of expectation and disappointment. Short-term price volatility commands attention, but the most consequential changes unfold quietly within the structure of the market itself.

What we are witnessing is not simply a price correction. It may represent a reallocation of capital as the digital asset market transitions toward its next stage of institutional maturity — a process that is uncomfortable in the near term and structurally significant over the long term.

RESEARCH METHODOLOGY

This report draws on the following data sources and analytical inputs:

– On-chain analytics platforms (Glassnode / CryptoQuant)

– ETF capital flow data (CoinGlass / Bloomberg)

– Major exchange public market data

– Public corporate disclosures (Strategy Inc. SEC Form 8-K, et al.)

– Research publications from Standard Chartered and JPMorgan

– Beta.B Group proprietary market analysis and expert interviews

RISK DISCLOSURE & DISCLAIMER

This report is produced for informational and analytical purposes only. It does not constitute financial advice, nor does it represent a solicitation or recommendation to buy, sell, or hold any financial instrument or digital asset. Investment in digital assets involves significant risk, including the potential loss of principal. All investment decisions should be made solely at the discretion and responsibility of the individual investor. Beta.B Group Limited makes no representations or warranties regarding the accuracy or completeness of third-party data cited herein.

ABOUT BETA.B GROUP LIMITED

Company | Beta.B Group |

Founded | 2017 |

Core Services | Web3 brand strategy · Cross-border PR Marketing (Japan, China, English-speaking markets) · Investor relations advisory · Market research & analysis |

Notable Clients | Nomura Securities, TON Foundation, OKX |

Website | |

Contact |

Comments